1.0

INTRODUCTION

The issue of gross domestic product (GDP) has become

topical as it forms the prime worry in the macroeconomics fraternity. Policy

makers and analysts are continually assessing the state of the economy since it

is perceived to be one of the primary aggregate indicators used to measure the

healthiness of any economy. Economic growth can be referred to as a sustained

increase in per capita national output or net national product over a

comprehensive period of time. A sustainable economic growth mainly rest on a

country’s ability to invest and make a well-organized and productive resource

endowment (Nyoni & Bonga,

2017f).

GDP per see does not reflect the

overall state of the standard of living or well-being of a country, however,

GDP per capita is often considered to reveal the condition of the average

citizen in any country. To this end, GDP per capita in Botswana recorded at 7523.22 US dollars

in 2017 which is equivalent to 60 percent of the

world's average. GDP per capita averaged 3427.73 USD from 1960 - 2017,

recording the highest rate of 7574.30 USD in 2014 and lowest of 390.80 USD in

1960 (tradingeconomics.com). During the same period, Botswana gained a high

middle income status as rated by the World Bank and UNDP Human Resource

Development Index (Maipose & Matsheka,

2009). In Africa, the country was ranked top in terms of governance and

transparency indices as reflected by political stability and

constitutional democracy (Honde & Abraha, 2015).

This

remarkable growth was attributed to prudent economic policies and mining

sector contributions, which proved to be an important variable of growth in

Botswana (IMF,2017). The sector contributed 24.5% to

the country’s GDP in 2013. This makes Botswana a success story of Africa, with

a strong government commitment to policies and a regulatory environment that

foster private sector development (Todaro, 2012).

Just like any other economy, the country requires a reliable, consistent and

accurate GDP forecasts to conduct a progressive monetary and fiscal policies.

Hence, this research attempts to model and forecast GDP per capita for the

period 1960-2017.

2.0

LITERATURE REVIEW

In comparing the

power of forecasting between ARIMA models and Artificial Neural Networks (ANN),

Okasha and Yaseen (2013)

agreed that the Box-Jenkins, ARIMA models proved to be more accurate than the

Artificial Neural Network (ANN) making it an alternative to the Box-Jenkins

approach. Using an econometric ANN model, Junoh

(2004) modeled and forecasted GDP growth in Malaysia (1995-2000), found out

that the ANN has an increased potential to predict GDP growth based on

knowledge-based economy indicators compared to the Box-Jenkins approach. Lu

(2009), in China; forecasted GDP using ARIMA models with annual data from 1962

to 2008 and noted that the ARIMA (4, 1, 0) model was the optimal model. In

India, Bipasha & Bani

(2012) forecasted GDP growth rates based on ARIMA models using annual data from

1959 to 2011 and established that the ARIMA (1, 2, 2) model was the optimal

model to forecast GDP growth in India. In Greece, Dritsaki

(2015) looked at real GDP basing on the Box-Jenkins ARIMA approach during the

period 1980 – 2013 and noted that the ARIMA (1, 1, 1)

model was the optimal model. In the case of Kenya, Wabomba

et al (2016); modeled and forecasted

GDP basing on ARIMA models with an annual data set ranging from 1960 to 2012

and concluded that the ARIMA (2, 2, 2) model was the optimal model for modeling

GDP in Kenya.

3.0

MATERIALS & METHODS

3.1 ARIMA

Models

ARIMA models are often considered as

delivering more accurate forecasts than econometric techniques (Song et al, 2003b). ARIMA models outperform

multivariate models in forecasting performance (du Preez

& Witt, 2003). Overall performance of ARIMA models is superior to that of

the naïve models and smoothing techniques (Goh &

Law, 2002). ARIMA models were developed by Box and Jenkins in the 1970s and

their approach of identification, estimation and diagnostics is based on the

principle of parsimony (Asteriou & Hall, 2007).

The mathematical formulation of the ARIMA (p, d, q)

model using lag polynomials can be simply written as:

4.1

Diagnostic Tests & Model Evaluation

4.1.1Stationarity

Tests: Graphical Analysis

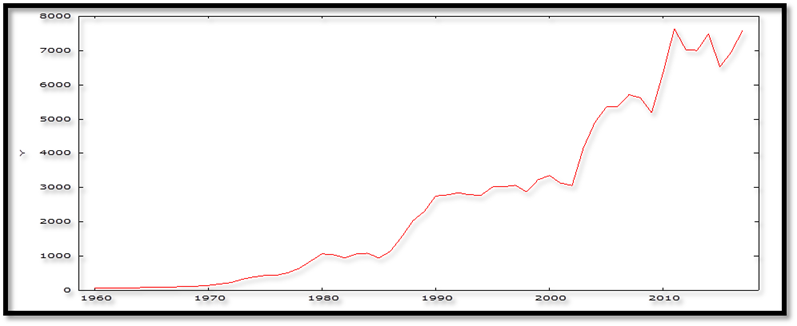

Figure 1

The Botswana GDP per capita variable, as

shown above is not stationary because it is trending upwards and this implies

that its mean is changing over time and thus its varience

is not constant over time.

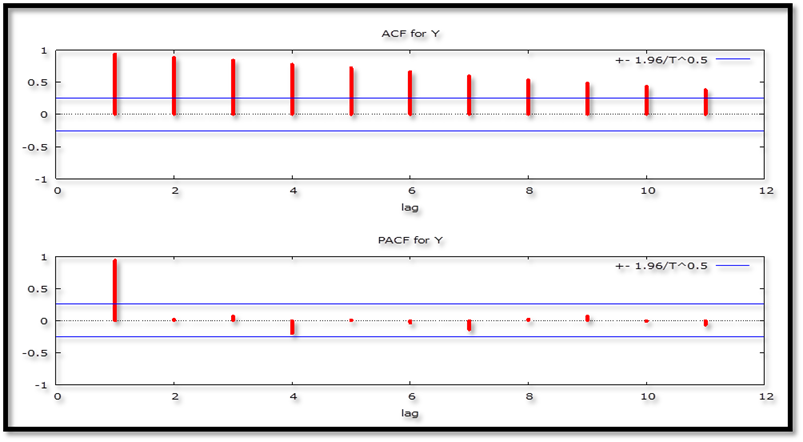

4.1.2 The Correlogram in Levels

Figure 2

4.1.3 The

ADF Test

Table 1:

Levels-intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

1.295578

|

0.9983

|

-3.560019

|

@1%

|

Not stationary

|

|

|

|

-2.917650

|

@5%

|

Not stationary

|

|

|

|

-2.596689

|

@10%

|

Not stationary

|

Table 2: Levels-trend

& intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

-2.022603

|

0.5766

|

-4.127338

|

@1%

|

Not stationary

|

|

|

|

-3.490662

|

@5%

|

Not stationary

|

|

|

|

-3.173943

|

@10%

|

Not stationary

|

Table 3: without

intercept and trend & intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

2.541447

|

0.9970

|

-2.606163

|

@1%

|

Not stationary

|

|

|

|

-1.946654

|

@5%

|

Not stationary

|

|

|

|

-1.613122

|

@10%

|

Not stationary

|

Figures 2 and tables 1 – 3, all indicate the non-stationarity of GDP per capita in levels. Thus Y is not I

(0).

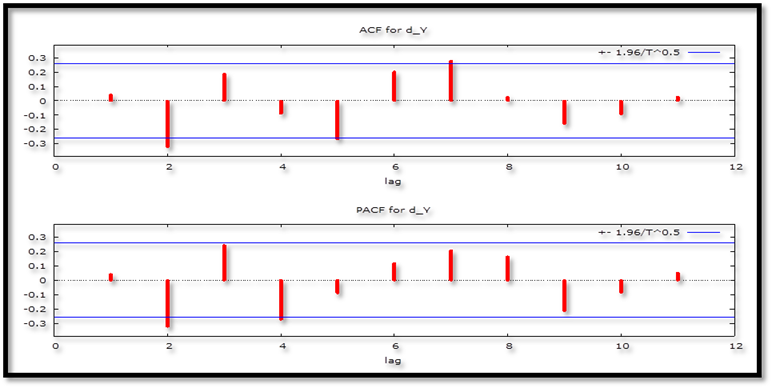

4.1.4 The Correlogram (at 1st Differences)

Figure 3

Table 4: 1st

Difference-intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

-4.503592

|

0.0006

|

-3.560019

|

@1%

|

Stationary

|

|

|

|

-2.917650

|

@5%

|

Stationary

|

|

|

|

-2.596689

|

@10%

|

Stationary

|

Table 5: 1st

Difference-trend & intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

-5.021871

|

0.0008

|

-4.140858

|

@1%

|

Stationary

|

|

|

|

-3.496960

|

@5%

|

Stationary

|

|

|

|

-3.177579

|

@10%

|

Stationary

|

Table 6: 1st

Difference-without intercept and trend & intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

Y

|

-2.882143

|

0.0047

|

-2.608490

|

@1%

|

Stationary

|

|

|

|

-1.946996

|

@5%

|

Stationary

|

|

|

|

-1.612924

|

@10%

|

Stationary

|

Figure 3 as well as tables 4 – 6, all show

that the Botswana GDP per capita series became stationary after taking first

differences; therefore, it’s I (1).

4.2 Evaluation of ARIMA models (without a

constant)

Table 7

|

Model

|

AIC

|

U

|

ME

|

MAE

|

RMSE

|

MAPE

|

|

ARIMA (1, 1, 1)

|

839.9019

|

0.89648

|

107.56

|

227.93

|

362.18

|

9.6045

|

|

ARIMA (2, 1, 1)

|

839.8412

|

0.94968

|

125.54

|

222.42

|

355.6

|

7.3849

|

|

ARIMA (3, 1, 1)

|

836.7766

|

0.87654

|

86.698

|

214.22

|

338.87

|

9.3593

|

|

ARIMA (4, 1, 1)

|

838.1568

|

0.88295

|

95.013

|

213.4

|

336.71

|

9.4365

|

|

ARIMA (4, 1, 0)

|

836.3743

|

0.88418

|

97.428

|

212.98

|

337.47

|

9.4365

|

|

ARIMA (3, 1, 0)

|

836.9577

|

0.87648

|

83.069

|

215.25

|

346.11

|

9.32248

|

|

ARIMA (0, 1, 1)

|

842.8361

|

0.85898

|

95.404

|

230.55

|

379.05

|

9.2927

|

|

ARIMA (0, 1, 2)

|

839.7101

|

0.91968

|

119.14

|

226.61

|

361.8

|

9.7583

|

|

ARIMA (2, 1, 2)

|

830.9423

|

0.88362

|

104.73

|

205.8

|

316.24

|

9.556

|

|

ARIMA (3, 1, 3)

|

830.887

|

0.81334

|

57.541

|

202.41

|

303.28

|

9.0468

|

A model with a lower AIC value is better

than the one with a higher AIC value (Nyoni, 2018n).

The research will only make use of the AIC in selecting the optimal model.

Thus, the ARIMA (3, 1, 3) model was preferred.

4.4

Residual & Stability Tests

ADF Tests

of the Residuals of the ARIMA (3, 1, 3) Model

Table 8:

Levels-intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

εt

|

-7.393910

|

0.0000

|

-3.562669

|

@1%

|

Stationary

|

|

|

|

-2.918778

|

@5%

|

Stationary

|

|

|

|

-2.597285

|

@10%

|

Stationary

|

Table 9: Levels-trend

& intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

εt

|

-7.459138

|

0.0000

|

-4.144584

|

@1%

|

Stationary

|

|

|

|

-3.498692

|

@5%

|

Stationary

|

|

|

|

-3.178578

|

@10%

|

Stationary

|

Table 10: without

intercept and trend & intercept

|

Variable

|

ADF Statistic

|

Probability

|

Critical Values

|

Conclusion

|

|

εt

|

-7.462036

|

0.0000

|

-2.610192

|

@1%

|

Stationary

|

|

|

|

-1.947248

|

@5%

|

Stationary

|

|

|

|

-1.612797

|

@10%

|

Stationary

|

The residuals of the chosen optimal model are

stationary as shown in tables 8 – 10.

4.5

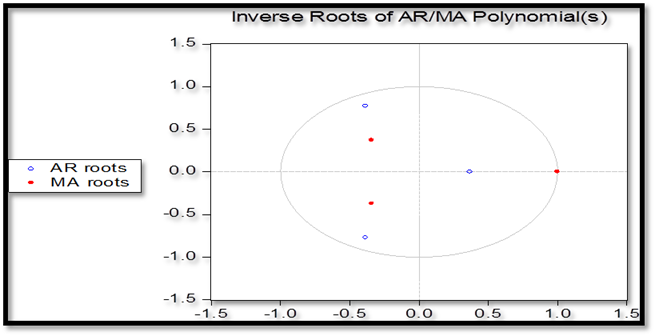

Stability Test of the ARIMA (3, 1, 3) Model

Figure 4

As illustrated in the figure above, the ARIMA

(3, 1, 3) model is stable as the corresponding inverse

roots of the characteristic polynomial lie in the unit circle.

5.0 FINDINGS

5.1

Descriptive Statistics

Table 11

|

Description

|

Statistic

|

|

Mean

|

2579.3

|

|

Median

|

2166.5

|

|

Minimum

|

58

|

|

Maximum

|

7646

|

|

Standard deviation

|

2453.9

|

|

Skewness

|

0.71616

|

|

Excess kurtosis

|

-0.77802

|

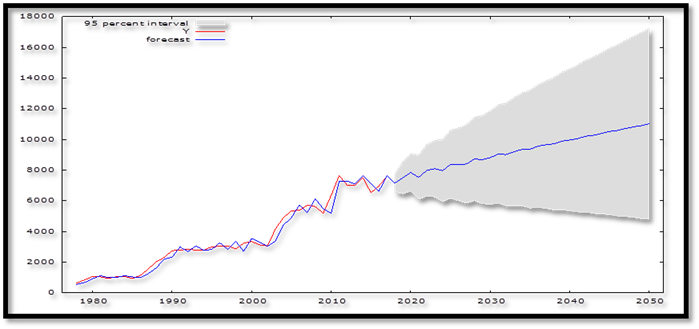

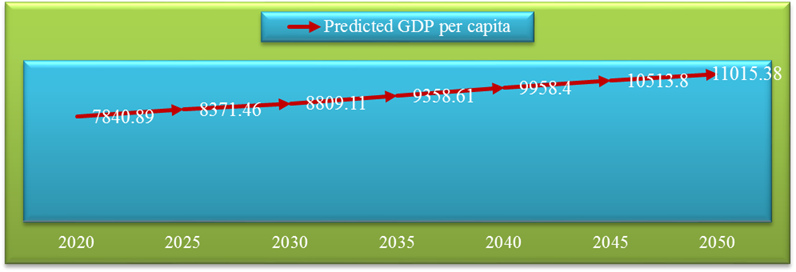

As portrayed in figures 5 and 6, Botswana is

now an upper middle income country, with a projected GDP per capita of

approximately 8809.11 USD by 2030. Botswana’s GDP per capita is on an upwards

trajectory which is expected to continue for at least 10 years. This clearly

proves beyond any reasonable doubt that the Batswana living standards will be

greatly improved and poverty levels are set to tumble low minimal levels with

the next decade. Indeed, Botswana; is an “African Success Story”, which can be

emulated by other African countries. It is important to note that a number of

factors have resulted in such a success story of Batswana. These include non-other-than good governance,

political stability and prudent macroeconomic management.

6.0 POLICY RECOMMENDATIONS

i.

The government of Botswana should maintain

the existing political stability and good governance, something which most

African countries always fail to do.

ii.

Botswana monetary authorities should continue

implementing the crawling peg exchange rate with preset basket weights because

it has indeed served the country well.

iii.

The government of Botswana should continue

working tirelessly to remove barriers to private sector – led growth I order to

increase the government revenue pool.

iv.

The country should use the rich diamond

reserves to diversify their economy.

7.0

CONCLUSION

Economic growth is always the priority of any

credible government around the globe (Adebayo, 2016) and in the case of

Botswana, successive governments have proved to be credible by being able to

conduct good governance and seriously prioritizing economic growth and price

stability ahead of selfish and politically motivated objectives. The continued

increase in GDP per capita in Botswana is clear testimony that Botswana is

indeed an “African Success Story” and is a good example of an African nation

where rule of law is a reality and corruption is an enemy of the society. The

results of this research are envisaged to help Botswana policy makers in

planning for an even brighter future for Batswana.

8.0

REFERENCES

1.

Adebayo, A. G (2016). Forecasting the Gross

Domestic Product in Nigeria using time series analysis and a sample frame of

1960 – 2015, Journal of Business and

African Economy, 2 (2): 1 – 14.

2.

Asteriou, D. &

Hall, S. G. (2007). Applied Econometrics: a modern approach, Revised Edition, Palgrave MacMillan, New York.

3.

Barhoumi, K., Darne,

O., Ferrara, L., & Pluyaud, B (2011). Monthly GDP

forecasting using bridge models: application for the French economy, Bulletin of Economic Research, 1 – 18.

4.

Bipasha, M & Bani,

C (2012). Forecasting GDP growth rates of India: an empirical study, International Journal of Economics and

Management Sciences, 1 (9): 52 – 58.

5.

Dritsaki, C (2015). Forecasting real GDP

rate through econometric models: an empirical study from Greece, Journal of International Business and

Economics, 3 (1): 13 – 19.

6.

Du Preez, J. & Witt,

S. F. (2003). Univariate and multivariate time series

forecasting: An application to tourism demand, International Journal of Forecasting, 19: 435 – 451.

7.

Goh, C. &

Law, R. (2002). Modeling and forecasting tourism demand for arrivals with

stochastic non-stationary seasonality and intervention, Tourism Management, 23: 499 – 510.

8.

Honde, G. J

& Abraha, F. G (2015). Botswana Economic Outlook

– Botswana, AfDB.

9.

International Monetary Fund (2017). Botswana Staff

Report for the 2017 Article IV consultation, IMF, Washington DC.

10.

Junoh, M. Z. H. J (2004). Predicting

GDP growth in Malaysia using knowledge-based indicators: a comparison between

Neural Network and econometric approaches, Sunway

College Journal, 1: 39 – 50.

11.

Lu, Y (2009). Modeling and forecasting China’s GDP

data with time series models, Department

of Economics and Society, Hogskolan Dalarna.

12.

Maipose, G.S and Matsheka, T.C (2009). The Indigenous Development State and

Growth in Botswana. Chapter 5. Volume 2: 01-66

13.

Nyoni, T & Bonga, W. G (2017f). An Empirical Analysis of the

Determinants of Private Investment in Zimbabwe, DRJ – Journal of Economics and Finance, 2 (4): 38 – 54.

14.

Nyoni, T & Bonga, W. G (2018a). What Determines Economic Growth In Nigeria?

DRJ – Journal of Business and Management,

1 (1): 37 – 47.

15.

Nyoni, T

(2018n). Modeling and Forecasting Inflation in Kenya: Recent Insights from

ARIMA and GARCH analysis, Dimorian Review, 5

(6): 16 – 40.

16.

Nyoni, T.

(2018i). Box – Jenkins ARIMA Approach to Predicting net FDI inflows in

Zimbabwe, Munich University Library –

Munich Personal RePEc Archive (MPRA), Paper No.

87737.

17.

Okasha, M.K and Yaseen, A.A (2013). Comparison Between

Arima Models And Artificial Neural Networks In

Forecasting Al-Quds Indices Of Palestine Stock Exchange Market. Conference

paper. Research Gate.

18.

Onuoha, D. O., Ibe,

A., Njoku, C., & Onuoha,

J. I (2015). Analysis of the Gross Domestic Product (GDP) of Nigeria: 1960 –

2012, West African Journal of Industrial

& Academic Research, 14 (1): 81 – 90.

19.

Song, H., Witt, S. F. & Jensen, T. C.

(2003b). Tourism forecasting: accuracy of alternative econometric models, International Journal of Forecasting,

19: 123 – 141.

20.

Wabomba, M. S., Mutwiri,

M. P., & Mungai, F (2016). Modeling and forecasting

Kenyan GDP using Autoregressive Integrated Moving Average (ARIMA) models, Science Publishing Group – Science Journal

of Applied Mathematics and Statistics, 4 (2): 64 – 73.